When it comes to investing in mutual funds, direct plans have generated a lot of attention in recent years. But a lot of people don’t know the difference between a direct and regular plan and which one they should choose. You’ve come to the correct location if you’re wondering the same things.

The primary distinction between a mutual fund scheme’s regular and direct plans is the way these plans are invested in and their respective fee structures.

A Regular Mutual Fund?

Investing through a middleman, such as a financial counsellor or a bank relationship manager, is part of regular plans. Since the fund firms must pay the intermediaries commissions, these plans typically have higher expense ratios when they are sold.

These programs are appropriate for investors who require ongoing advice and help from a financial professional.

Differences Between Regular and Direct Mutual Fund Plans

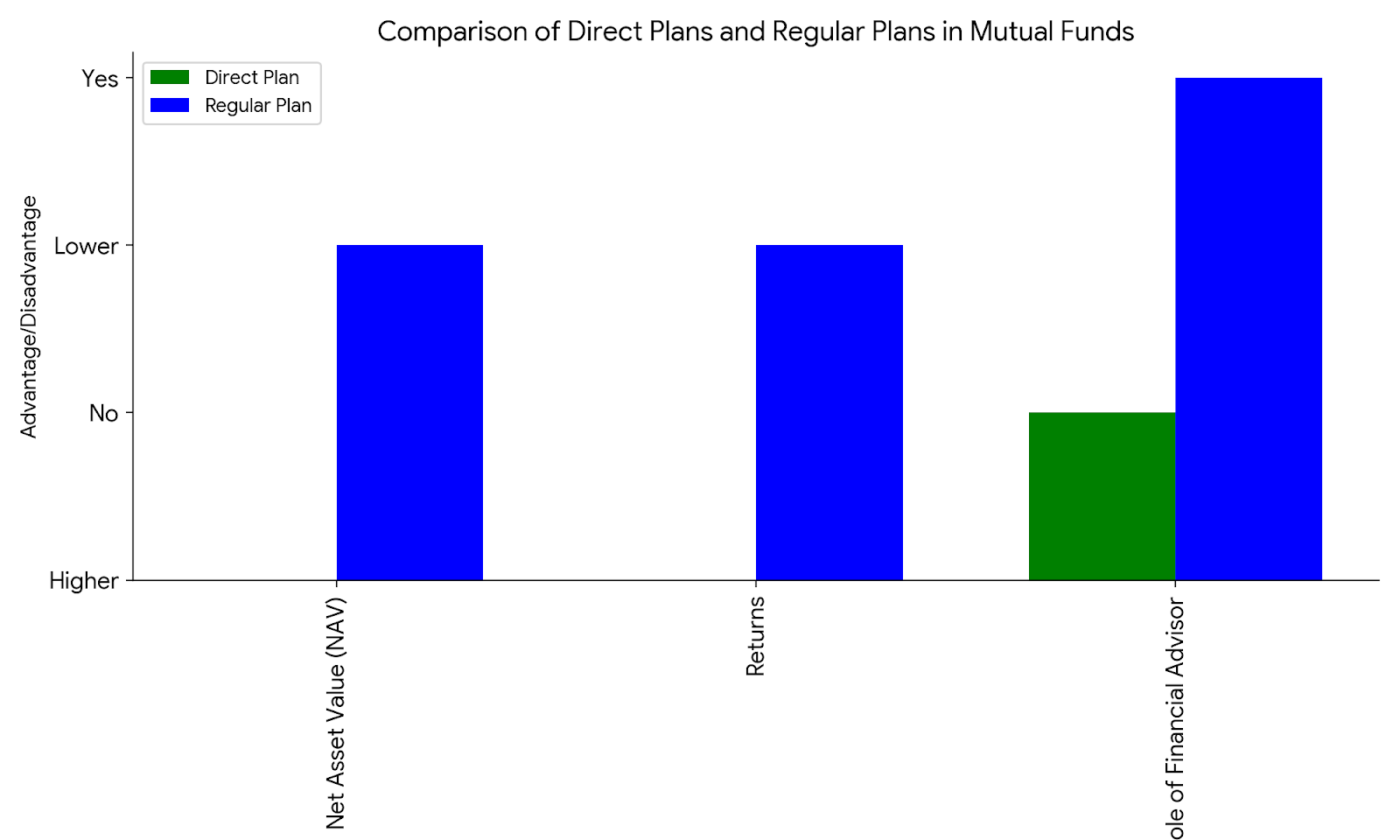

Any mutual fund scheme has two variations: direct plans and regular plans. These variations are based on how you invest in the mutual funds. Therefore, it’s critical to comprehend how they differ from one another. Based on Net Asset Value (NAV), Returns, and the Financial Advisor’s Role, the following are some of the main differences:

Value of Net Assets: Fund houses deduct various management costs from the fund’s net asset value (NAV). We call this the expense ratio. Since there is no fee or brokerage in direct plans, the NAV of regular schemes is typically lower than that of direct plans, which have a higher expense ratio because of the commission and brokerage associated with the regular fund.

Returns: Because they have a lower expenditure ratio than ordinary funds, direct plans provide higher returns. Higher profits are achieved by excluding distributor commissions, which is advantageous to you. Regular plans, in contrast to direct plans, have a greater expenditure ratio that reduces your return and provide somewhat lower returns.

The Financial Advisor’s Role: You engage with the asset management business directly when you have a direct plan. There is no role for a financial counsellor because you invest in this program following your requirements and decisions. Regular plans, on the other hand, involve financial experts helping you with the investing process. By your investing goals, they assist you in determining where and how much to invest.

Regular Mutual Fund Benefits

There are benefits to both regular and direct mutual fund programmes, although regular funds have some advantages for some clients. Regular funds have the following advantages versus direct funds:

Assistance from Financial Advisors: Financial advisors assist you in selecting appropriate funds for your regular fund investments depending on your investment goals and risk tolerance. Therefore, consistent funding will be beneficial to you if you are a novice investor in need of ongoing guidance and support.

Frequent observation: With direct funds, it is your responsibility to keep an eye on the fund’s performance; with regular funds, on the other hand, your financial advisor keeps an eye on your portfolio, assesses it, and makes recommendations for adjustments as needed.

Which is Preferable, Regular Mutual Funds or Direct?

Below table compares Regular and Direct Mutual Funds to help you decide which one is right for you:

| Feature | Regular Funds | Direct Funds |

| Suitability | Investors seeking guidance & assistance | Investors comfortable with self-directed investing |

| Investment Approach | Financial advisor helps create a goal-based plan | Independent research and decision-making |

| Expense Ratio | Higher (includes commission & brokerage) | Lower (no commission or brokerage) |

| Returns | Potentially lower due to higher expense ratio | Potentially higher due to lower expense ratio |

| Cost-Effectiveness | Lower | Higher |

| Financial Advisor Involvement | Yes, advisor provides guidance | No, investor manages directly |

Therefore, you can move forward with regular funding if you require ongoing assistance and direction from a professional advisor. Direct funds, on the other hand, are a more affordable option if you want to maximise your long-term gains and pay no commissions or brokerage fees.

Identifying Direct vs. Regular Mutual Funds

Many investors make the mistake of choosing the wrong option because they are unsure about the differences between regular and direct funds. The following are some crucial characteristics that can assist you in determining whether funds are direct or regular:

- Fund Name: The term “Regular” or “Reg” appears in the mutual fund scheme name for regular funds. Similar to this, the scheme name for direct money includes the words “Direct” or “Dir.”

- Cost-to-Rate: Both plan types’ expense ratios are available for inspection. Regular plans typically have a greater cost-to-income ratio than direct plans.

- Net Asset Value (NAV): The fund’s NAV is also available for inspection. Direct plans typically have a higher net asset value (NAV) than ordinary plans.

- Consolidated Account Statement (CAS): To find out if a mutual fund is regular or direct, you can also review your CAS. In your CAS, look for the “Advisor” field. In this area, you’ll see ‘ARN’ followed by a number if the plan is regular.

Conclusion

Now that you understand the key differences between Regular Funds and Direct Funds, you can make an informed decision about which one is right for you. Remember, even a small difference in expense ratio can significantly impact your returns over time. For personalized guidance and to explore the best investment options for your goals, consider contacting a professional financial advisor.

Looking for the best mutual fund investment app or a trusted advisor to guide you through your investment journey? We can help! Contact us today to get the best consultation and explore how we can assist you in achieving your financial goals.